(1).png)

The Pakistan Stock Exchange (PSX) extended its bullish momentum on Tuesday, with the benchmark KSE-100 Index posting a sharp gain as investors remained encouraged by positive developments surrounding the FY2026-27 federal budget, easing geopolitical tensions in the Gulf region, and expectations of continued macroeconomic stability.

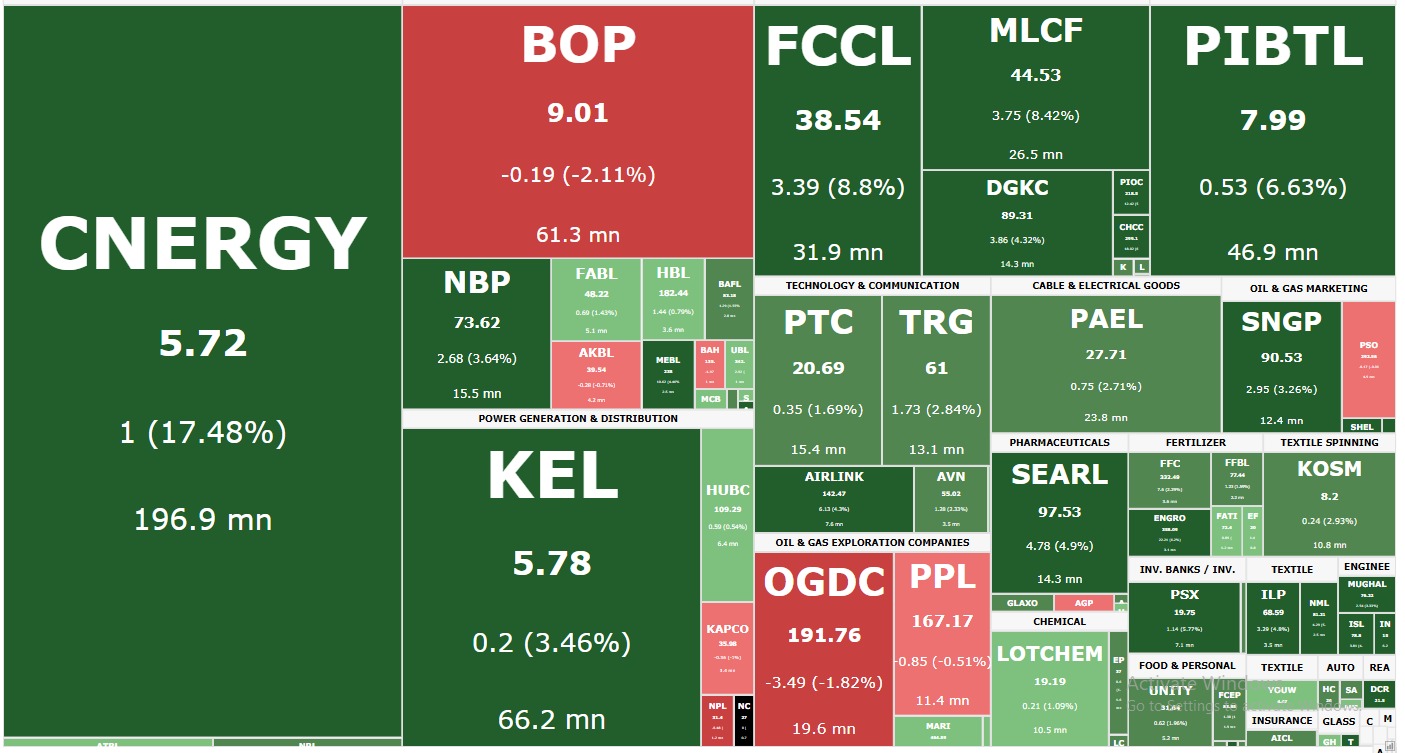

The KSE-100 Index settled at 180,392.97, registering a gain of 3,353.15 points (+1.89%). The benchmark remained firmly in positive territory throughout the trading session, reaching an intraday high of 180,503.55 (+3,463.73 points) and a low of 177,741.46 (+701.64 points), reflecting sustained buying interest across key sectors.

Trading activity remained strong, with total volume in the KSE-100 Index recorded at 610.92 million shares, highlighting robust investor participation.

Market breadth remained highly positive, with 81 companies closing higher and only 19 ending the session lower, indicating broad-based strength across the benchmark index.

Among the top gainers, SSGC (+10.01%), SNGP (+10.00%), PSX (+10.00%), PABC (+6.72%), and UBL (+6.16%) posted notable advances. On the downside, PGLC (-2.93%), JVDC (-2.90%), IBFL (-2.23%), BNWM (-2.21%), and DGKC (-1.75%) were among the major decliners.

In terms of index-point contribution, UBL led the rally by adding 807.82 points to the benchmark index, followed by ENGROH (+330.44 points), BAHL (+234.62 points), NBP (+147.65 points), and PPL (+143.02 points). Meanwhile, DGKC (-29.56 points), JVDC (-29.50 points), ILP (-11.76 points), KOHC (-9.16 points), and PSEL (-8.75 points) weighed on the index.

Sector-wise, Commercial Banks remained the primary driver of gains, contributing 1,839.22 points to the benchmark index. Additional support came from Investment Banks, Investment Companies & Securities Companies (+410.98 points), Oil & Gas Exploration Companies (+232.34 points), Oil & Gas Marketing Companies (+187.32 points), and Fertilizer (+146.18 points). Limited pressure was observed from Property (-29.50 points), Cement (-9.03 points), Engineering (-3.39 points), Synthetic & Rayon (-2.95 points), and Woollen (-0.26 points).

Investor sentiment remained upbeat as market participants continued to welcome the business-friendly measures announced in the FY2026-27 federal budget. Relief in super tax, lower withholding taxes on property transactions, reduced advance tax for exporters, and the continuation of incentives for the IT sector strengthened expectations of improved corporate profitability and economic growth.

Market confidence was further boosted after U.S. President Donald Trump announced that a preliminary agreement had been signed between the United States and Iran aimed at ending tensions in the Gulf region. The development eased concerns regarding potential disruptions to global energy supplies and improved overall risk appetite among investors.

Additionally, sentiment received support from the State Bank of Pakistan's Monetary Policy Committee decision to keep the policy rate unchanged at 11.5% during its June 15, 2026 meeting. The decision reinforced confidence in the country's improving economic outlook and provided greater clarity on the future interest-rate environment, benefiting banking, energy, and other cyclical sectors.

In the broader market, the All-Share Index closed at 108,164.80, gaining 1,725.65 points (+1.62%). Total market volume increased to 1.22 billion shares from 988.08 million shares in the previous session, while traded value rose to Rs70.22 billion.

A total of 612,215 trades were reported across 496 companies, with 303 advancing, 165 declining, and 28 remaining unchanged, reflecting strong participation across the wider market.

Top volume leaders included LOTCHEM (108.12 million shares), PIBTL (49.52 million), STPL (43.73 million), SSGC (42.98 million), and KEL (40.12 million shares).

-surges-to-rs44.23-trillion-as-bank-deposits-jump)

-falls-weekonweek-to-rs40.95tr)

-ltd-reports-strong-halfyearly-results-–-profit-surged)

)

Add a comment