(1).png)

The Pakistan Stock Exchange (PSX) remained under pressure on Tuesday as persistent profit-taking in heavyweight banking and fertilizer stocks outweighed gains in the energy sector, pushing the benchmark KSE-100 Index lower for a second consecutive session.

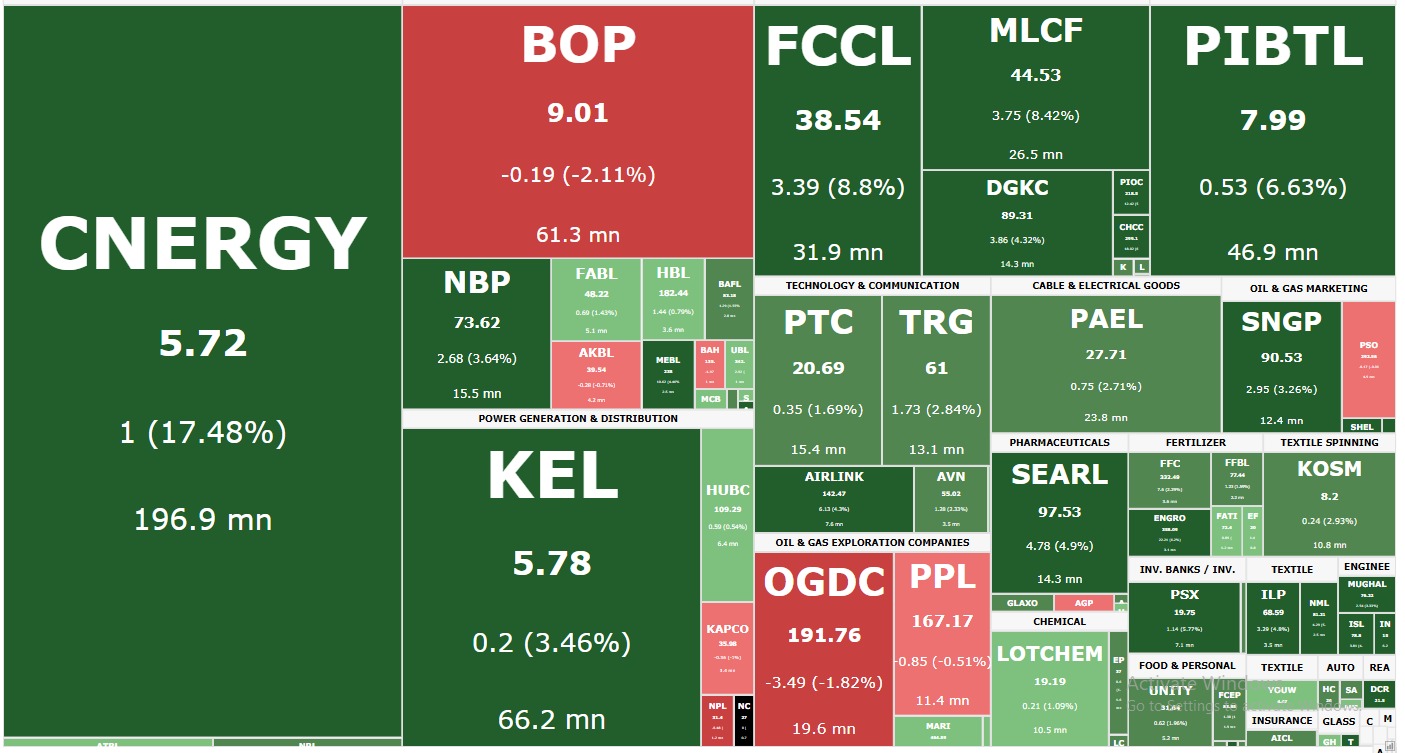

The KSE-100 Index settled at 177,692.92, declining by 778.94 points (-0.44%). After opening on a positive note, the benchmark failed to sustain early gains and reversed course during the latter half of the session. The index traded within a range of 1,731.18 points, reaching an intraday high of 179,405.55 (+933.69 points) before falling to a low of 177,674.37 (-797.49 points).

Investor sentiment remained cautious despite continued optimism surrounding ongoing diplomatic efforts between the United States and Iran. While hopes for a formal peace agreement helped keep international oil prices relatively contained, investors opted to lock in profits in major banking stocks following the market’s strong rally in recent weeks.

The Commercial Banks sector emerged as the primary drag on the benchmark index, with significant selling pressure observed in large-cap names including UBL, BAHL, and BAFL. Profit-taking also extended to fertilizer, automobile, and technology stocks, limiting the market’s ability to maintain its early-session momentum.

Meanwhile, oil and gas exploration companies continued to attract investor interest. The sector provided meaningful support to the benchmark amid lingering geopolitical uncertainty in the Middle East and expectations of stable earnings from energy-related companies.

Market breadth remained weak, with 71 companies closing lower, 28 advancing, and one remaining unchanged among the KSE-100 constituents.

Among the major decliners, SSOM (-5.91%), GHGL (-5.42%), MEHT (-3.96%), BAHL (-2.63%), and HCAR (-2.62%) recorded significant losses. On the positive side, KEL (+2.68%), MLCF (+2.52%), SNGP (+2.28%), SSGC (+2.20%), and COLG (+2.07%) emerged as the session’s top performers.

In terms of index-point contribution, UBL exerted the largest negative impact on the benchmark, erasing 249.76 points. Other major contributors to the decline included BAHL (-130.86 points), ENGROH (-90.95 points), FFC (-63.65 points), and BAFL (-59.06 points).

On the positive side, OGDC contributed 88.42 points to the benchmark index, followed by MLCF (+41.86 points), PPL (+39.56 points), SNGP (+24.84 points), and COLG (+22.03 points), helping offset part of the broader market weakness.

Sector-wise, Commercial Banks remained the biggest drag on the index, shaving off 608.83 points. Additional pressure came from Investment Banks, Investment Companies & Securities Companies (-97.34 points), Fertilizer (-94.32 points), Automobile Assemblers (-64.16 points), and Technology & Communication (-53.96 points).

Support came primarily from Oil & Gas Exploration Companies (+123.61 points), followed by Cement (+54.00 points), Food & Personal Care Products (+28.84 points), Oil & Gas Marketing Companies (+20.41 points), and Leather & Tanneries (+15.94 points).

In the broader market, the All-Share Index settled at 107,527.39, declining by 222.76 points (-0.21%). Total market volume stood at 765.14 million shares compared to 807.47 million shares in the previous session, while traded value decreased to Rs35.44 billion.

A total of 409,228 trades were reported across 493 listed companies. Of these, 146 companies closed higher, 308 declined, and 39 remained unchanged, indicating continued weakness across the wider market.

Top volume leaders during the session included KEL (83.43 million shares), WTL (71.24 million shares), SSGC (32.35 million shares), FNEL (30.73 million shares), and TPL (23.48 million shares).

Closing Summary – 23 June 2026:

The Pakistan Stock Exchange extended its decline for a second consecutive session as persistent profit-taking in banking and fertilizer stocks continued to weigh on investor sentiment. Although energy stocks provided support amid expectations of stable sector earnings and ongoing geopolitical developments, losses in major banking names dominated market direction. The benchmark KSE-100 Index closed 779 points lower at 177,692.92, reflecting a cautious investor approach following the market’s recent rally. On a cumulative basis, the KSE-100 Index has gained 52,066 points (+41.44%) during the current fiscal year and remains higher by 3,639 points (+2.09%) on a calendar year-to-date basis.

-surges-to-rs44.23-trillion-as-bank-deposits-jump)

-falls-weekonweek-to-rs40.95tr)

-ltd-reports-strong-halfyearly-results-–-profit-surged)

)

Add a comment